Note: This blog post is the second in a four-part series exploring how Root Capital measures and manages the impact of our lending. Read parts one, three, and four.

Agricultural enterprises are changemakers in rural communities. They have the ability to improve livelihoods, conserve the environment, and generate opportunities for women and young people. To be a force for good, however, these enterprises must adopt sound business practices that are sustainable, inclusive, and financially responsible.

As an impact-first lender, Root Capital wants to support these changemakers. But how do we make sure we are investing in businesses that don’t just avoid harmful practices, but actually drive high-impact change in their communities?

Measuring likely enterprise impacts

To ensure we’re partnering with enterprises that advance our mission, we need an ex-ante system—which we call social and environmental due diligence—that assesses the likely positive and negative impacts of each potential borrower. This social and environmental due diligence occurs alongside our credit due diligence. During this process, we screen out enterprises that engage in practices that damage human or environmental health (e.g., deforestation of protected areas) and prioritize those that engage in practices likely to improve livelihoods or preserve local ecosystems.

We say “likely” because our social and environmental due diligence process largely relies on a “practices as proxies” approach, using business practices that—according to industry research and our own impact studies—are associated with better outcomes for rural communities.

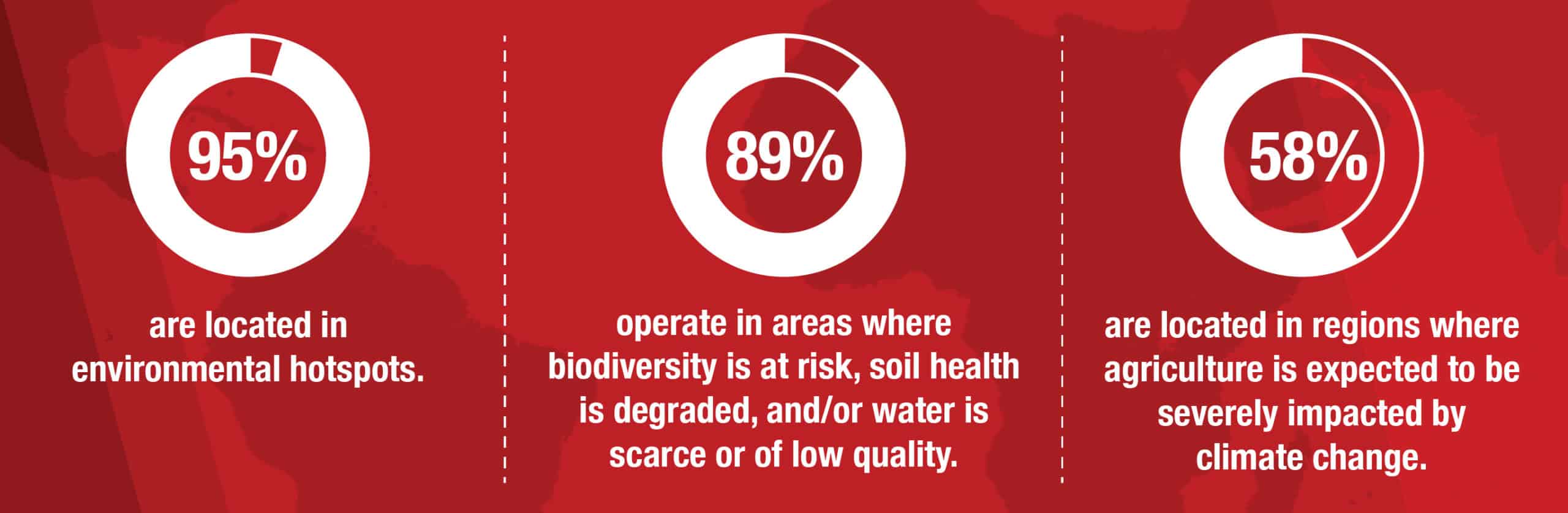

In 2018, almost all of our clients were located in environmental hotspots.

In 2018, almost all of our clients were located in environmental hotspots.

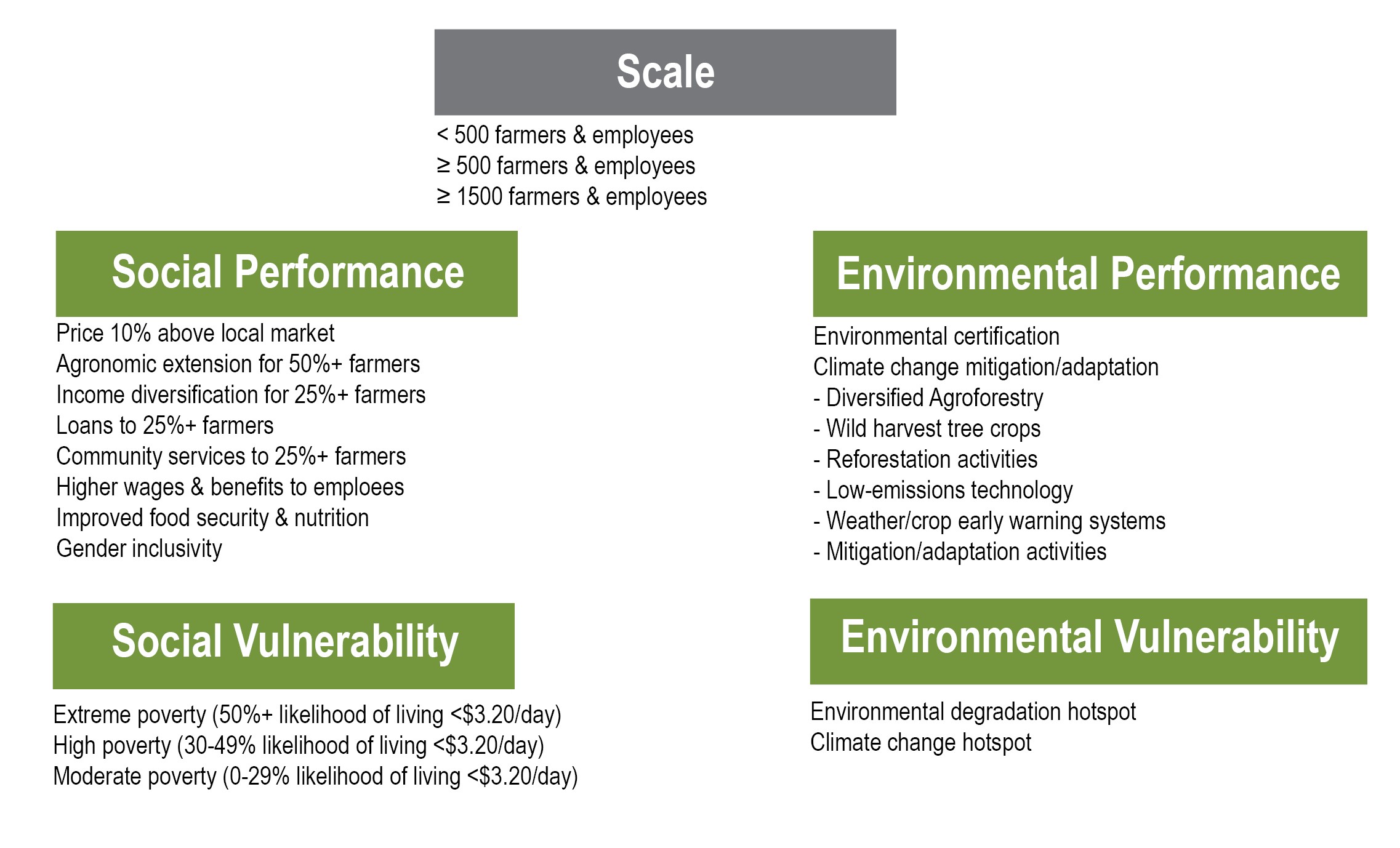

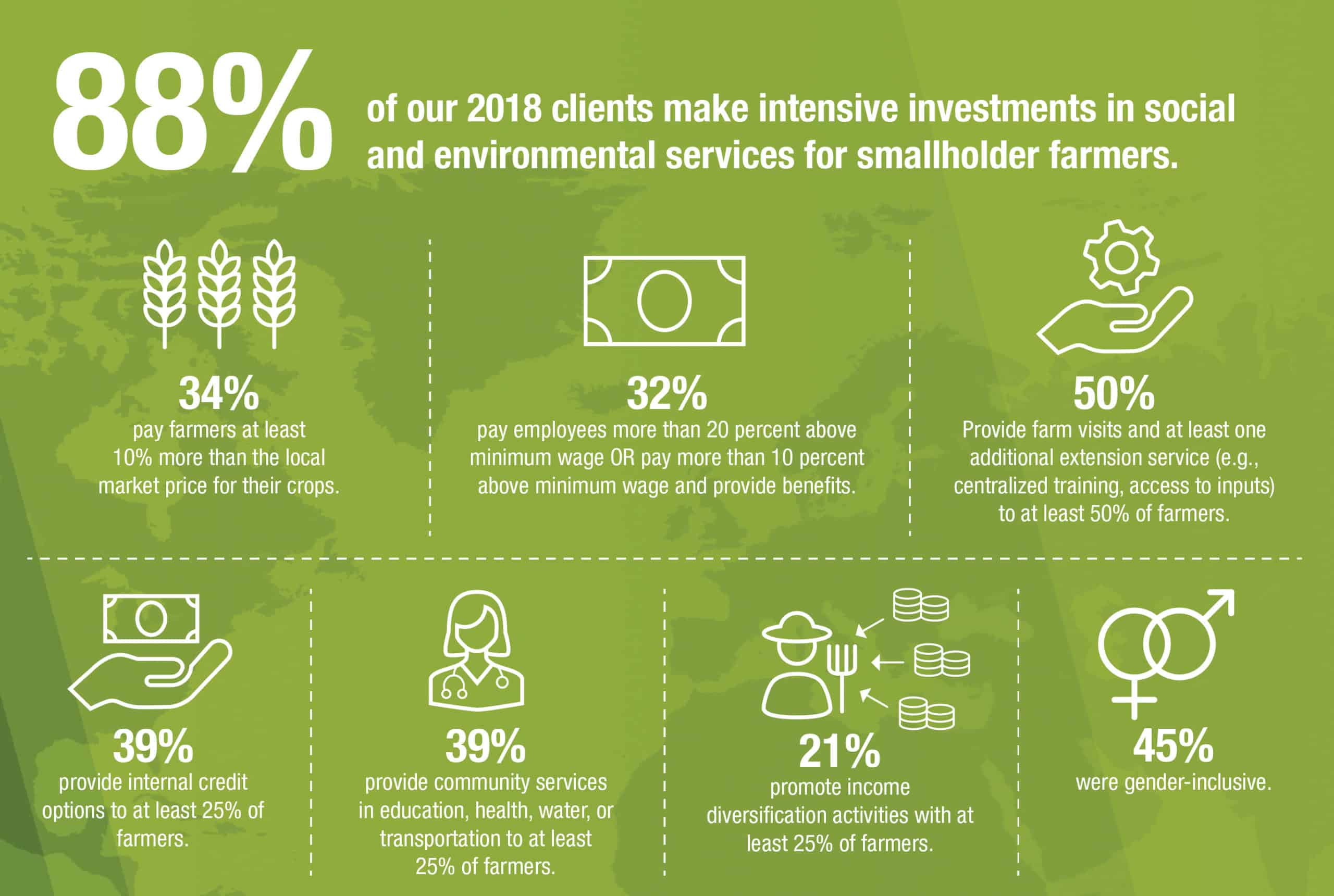

For each potential loan and borrower, we look at more than two dozen of these impact proxies; a full list of which can be seen below. We start by assessing the level of need in the communities where the enterprise works. We evaluate both social vulnerability—measured through the local level of poverty—and environmental vulnerability, which we gauge by looking at the degree of ecosystem degradation and the predicted effects of climate change on the region. We then assess a businesses’ commitment to addressing these conditions through social and environmental services, such as price premiums for farmers, benefits to employees, or reforestation projects.

We apply an intensity threshold to each service to identify businesses making deep investments in their communities. For example, we only count a price premium to farmers if it is more than 10 percent above the local market price.

Measuring likely investment impacts

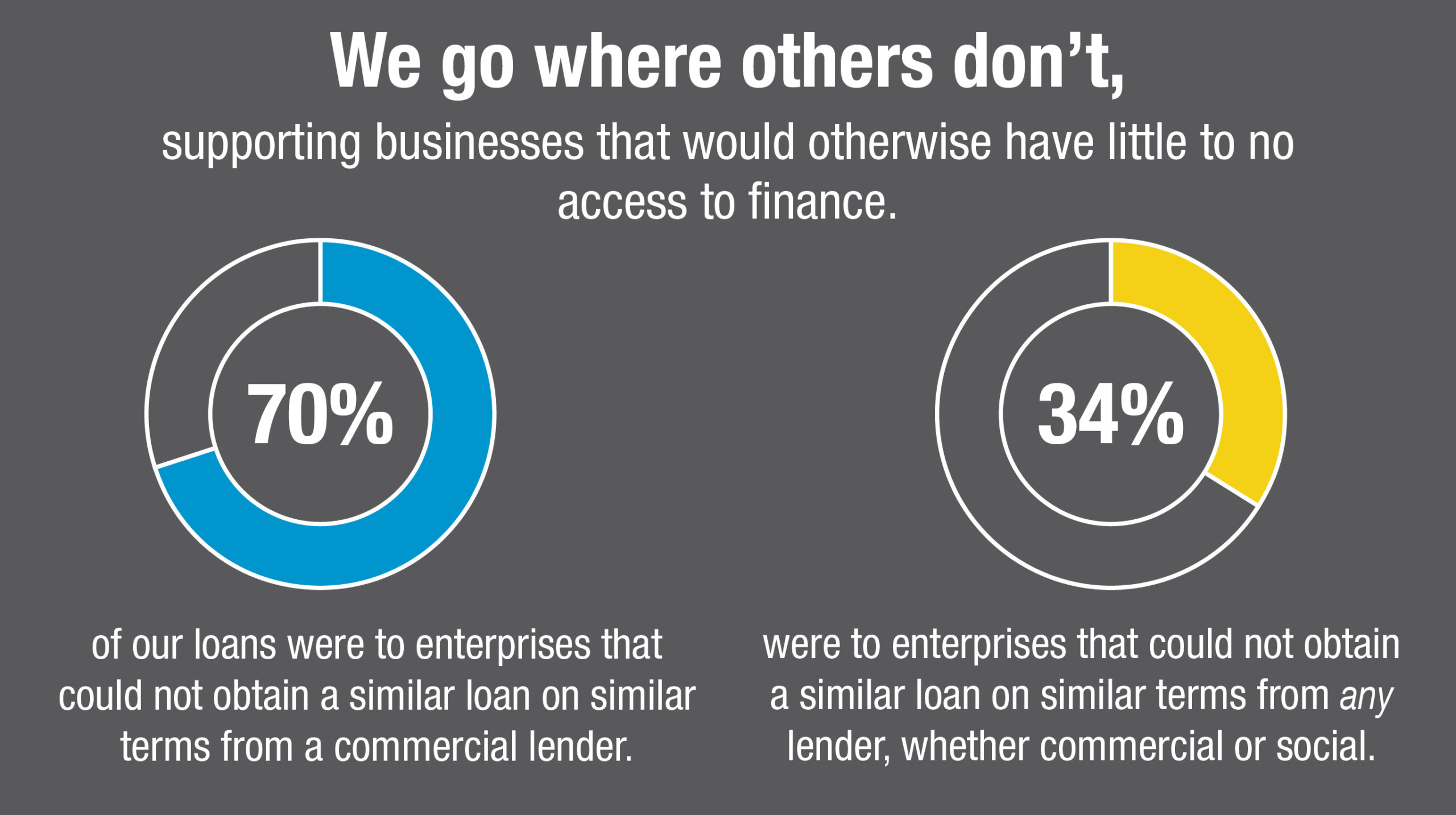

Once we’ve identified a high-impact business, we also want to understand the likely impact of our loan on that business.

Here, we use the concept of “additionality,” a measurement of what our loan would provide the enterprise beyond what other lenders would have provided in our absence. To evaluate the additionality of a proposed loan, we ask the question: Could this business likely obtain a similar loan on similar terms from another source? And if so, from what kind of source—another impact-first lender or a commercial lender?

Measuring loan additionality is one of the most challenging parts of our social and environmental due diligence process. It requires our loan officers to make difficult judgments about alternative lending options in a particular market and whether or not those options are available to a particular business. But it is also one of the most important ways that we manage toward a high-impact portfolio. Our loan officers are equipped to make these judgments because they are embedded in the communities and markets where they work. They have a deep understanding of the local agricultural industry and credit market. That knowledge—combined with other information like detailed client financial statements—provides our loan officers the information they need to make these important determinations.

Managing toward greater impact

After collecting data on the likely impacts of each borrower and potential loan, we synthesize the information through an internal tool called the Expected Impact Rating. This allows us to quantify and compare the likely impacts of our lending across our global portfolio—not as an academic exercise, but to inform decision making.

As an impact-first lender, we want to prioritize loans that are additional to high-impact businesses. Yet these additional loans are often smaller in size and for earlier-stage businesses that don’t have experience with formal borrowing. As such, they often carry more risk, earn less revenue, and require more resources to underwrite and monitor. Rather than pass these costs on to our borrowers—whose operations would be devastated by high interest rates—we offer rates and fees that rural enterprises can afford, while seeking philanthropic support to cover the gap. These lower rates and fees are still competitive with local lenders and in line with our goal to crowd in the local market, not distort it. Still, we cannot afford to make every additional loan that crosses our desk. Therefore, we use the Expected Impact Rating to identify and prioritize the highest-impact loans that Root Capital can afford to make. This approach allows us to manage toward topline impact objectives across a portfolio of 200+ loans a year.

![[YOUTH] HN_hawkey_COCAOL_20120223_046](https://rootcapital.org/wp-content/uploads/2019/12/YOUTH-HN_hawkey_COCAOL_20120223_046-scaled-2.jpg)

Evaluating the actual impact of our loans

Our social and environmental due diligence process allows our lending team to measure and manage toward impact in real time, as we review new loan opportunities each day.

However, because these due diligence tools rely on proxy practices, they cannot ensure that the predicted outcomes will occur, nor can they definitively attribute positive impact to the loan—a key element of impact evaluation. Returning to the example of price premiums, a business’ higher payments to farmers may or may not directly translate to improved outcomes for farming families, such as greater income.

This is where our impact evaluations come in. Each year, Root Capital conducts deep-dive evaluations with a subset of our borrowers to test our assumptions about what actually drives impact for rural communities. In the next installment of this series, we’ll take a look at our ex-post studies, which allow us to compare our predicted impact with the actual impact of our loans and borrowers. These studies, in turn, inform our social and environmental due diligence so that we can continue to identify agricultural businesses that will improve rural livelihoods.

Read parts one, three, and four of this four-part series exploring how Root Capital measures and manages the impact of our lending.

Note: This post includes content or concepts that originally appeared in “Toward the Efficient Impact Frontier,” by Michael McCreless, Stanford Social Innovation Review, Winter 2017.

Photos © Sean Hawkey and Root Capital